In search of things new and useful.

Traction vs. Product

I’ve had a couple conversations with other investors recently around what a seed stage company needs to achieve to raise a series A. This is something we think a lot about given that we are exclusively seed stage investors, and we’ve written a fair bit about it in the past (see here for a data driven post on the seed to series A dynamics in our portfolio).

Often, I find that there is a very distinct trade-off that surfaces when thinking about how to best position yourself for your series A:

Option 1 is to focus nearly exclusively on some traction metric. For most companies, this means top-line revenue, but in some cases it’s more about numbers of active users or number of customers. This is in line with the YC adage that “growth solves (nearly) all problems”. Under this strategy, things get sacrificed in favor of growth. You might do unscalable, hacky things to get customers. You might do tons of stuff manually to fulfill the promise of your service instead to taking more time and using more resources to build software. You will probably make decisions to sacrifice margin for growth.

Option 2 is to focus on product (and proof points more broadly). What are the risks of your business and have you found ways to address those risks or eliminate them altogether? You probably are quicker to build technology vs throwing bodies at a problem. You are searching for stuff that is repeatable and scaleable. You focus on finding very strong PMF and building a small scale machine.

The traction strategy might end up failing at the series A because investors dig beneath the covers and see that despite the growth, there are a bunch of risks underneath that haven’t really been addressed. Also, in a market where a bunch of high-flyers are crumbling, investors are more deliberate and less enamored by pure top line metrics. This strategy can also fail because the goal line might move. $1M ARR used to get a series A done, but now it’s more like $3M. $5M in ecommerce revenue or marketplace GMV used to be interesting, but now it’s more like $10M. Etc.

The product and proof strategy might also fail at the series A. Many investors may appreciate all your methodical work, but still feel like it’s hard to pull the trigger without more traction. Very proven repeat founders can usually get away with early proof points even with limited top-line growth, but most teams will feel like they are approaching investors from a weak position if the headline numbers don’t pop. This is especially true in markets that are out of favor or unsexy (or where investors feel out of their comfort zone).

It’s a tough trade-off. IMHO, the best way to maximize one’s chances of getting a series A done is to focus on traction. You definitely need to clear the goal posts, and if you do, I think 9 times out of 10, you will raise a series A. It might be tough and you might need to run a broad process, but I think that with impressive traction, you are likely to find a true believer that the other stuff can be worked out.

But… I think the best way to build a great business is to focus on product and proof. The early stage of a business is when everything is a blank canvas and you have maximum agility. It’s much harder to morph your product and business when you are already running at 75 miles per hour with a big team than when you are a small group that is just getting started. You will be more likely to make bad decisions at that point because you will feel loss aversion and a ton of pressure to maintain or accelerate your growth. The investors that you have convinced to do the series A are the very ones that believed that you were doing things the right way, which will make it even harder to change course. Some founders are able to do this, but most end up struggling, or doing it way too late.

Obviously, the best path is to do both, but that’s not very helpful 🙂 My advice is typically to keep teams really small after the seed round to prove as much as you can, even if it takes longer. You raise money assuming 12-18 months runway with some ramp in hiring, but for the first 3-6 months, you should have a burn level that could probably last you 2.5-3 years if needed. Then when you feel like you have some of the major risks worked out, grow as fast as you can. Investors do care about absolute levels of traction, but they care almost as much about the steepness of the curve and the shape of that traction.

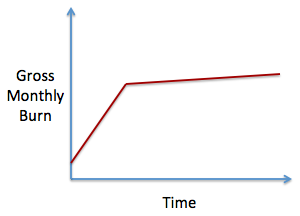

Instead, what I often see is that the minute seed money is in the bank, founders try to staff up very quickly. They feel like they have a relatively big war chest, and the returns of having great people will compound over time (and it will be easier to bring on great people when you have just raised funding). So, they get pretty close to their target team size that gets them 12-18 months runway out of the gate, and their gross burn looks something like this:

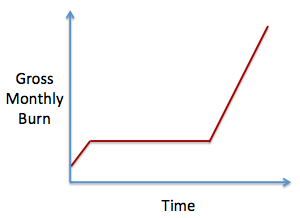

Instead, many of our best performing companies grew their team very modestly immediately after the seed and worked on finding strong PMF with that small team. Once they were confident that things were really starting to work, they stepped on the gas aggressively, both increasing their gross burn but also showing a steep growth curve. Their curves looked more like this:

In a number of cases, this approach actually led to pretty fast series A’s, and ones that occurred pre-emptively when there was still 6+ months of cash in the bank, which is the best place to be when you are raising capital.